As part of the analysis for our annual State of Commercial Banking webinar and report, we look into commercial loan demand, what happened in the previous 12 months and what factors are shaping the outlook for the coming months.

The executive brief version of what we found: 2021 was rough, but there are reasons why 2022 may be looking up for getting more commercial loans on the books.

A reminder that the data in this blog post, and in the State of Commercial Banking webinar and report, is pulled primarily from Q2’s proprietary databases. The Q2|PrecisionLender databases reflects actual commercial relationships (loans, deposits, and other fee-based business) from more than 150 banks and credit unions in the United States, ranging in size from small community banks to top 10 U.S. institutions. In addition to the actual relationship data, we gleaned insights from RM pricing activity on the Q2|PrecisionLender platform.

The 2021 Story: A Lot of Effort, but Even More Liquidity

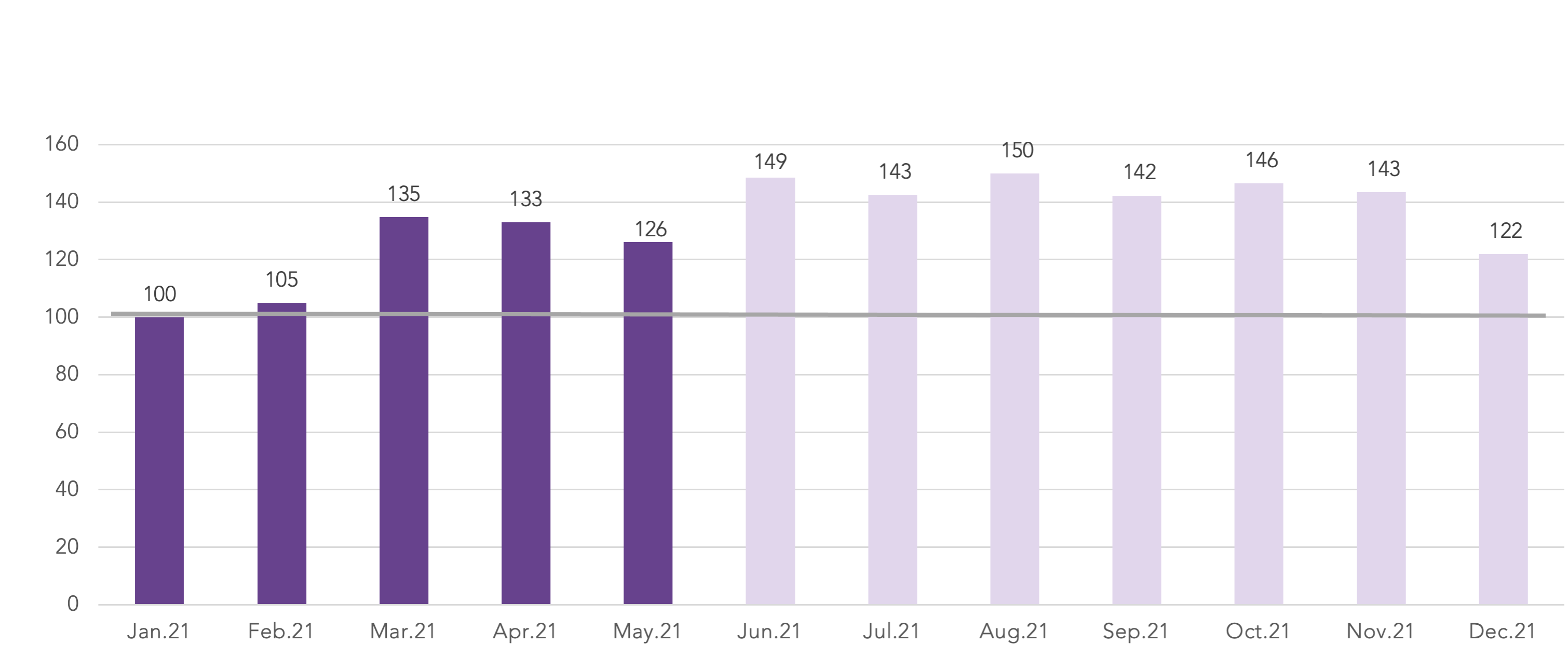

Commercial banking leaders told us early in 2021 that increasing commercial loan volume was a priority for them. Financial institutions were flush with capital, feeling more optimistic about credit to put their funds to work. Beginning in March we began to see that reflected in pricing activity. In the second half of 2021, Q2 clients priced nearly 50% more volume than at the start of the year.

Figure 1: Bankers Step Up Commercial Pricing Activity

Priced Commercial Loan Volume, by Month

Source: Q2|PrecisionLender. Analysis reflects volume of deals priced on the PrecisionLender platform, indexed to 100 for January 2021.

Clearly banks were more active. But it’s important to remember the chart above shows pricing activity, not actual loans that ended up on the books in 2021. Federal Reserve H8 numbers showed that C&I loan volume fell in 2021, while CRE loan volume rose, but modestly.

So why didn’t the increased efforts from banks bear fruit?

A Glut of Deposits

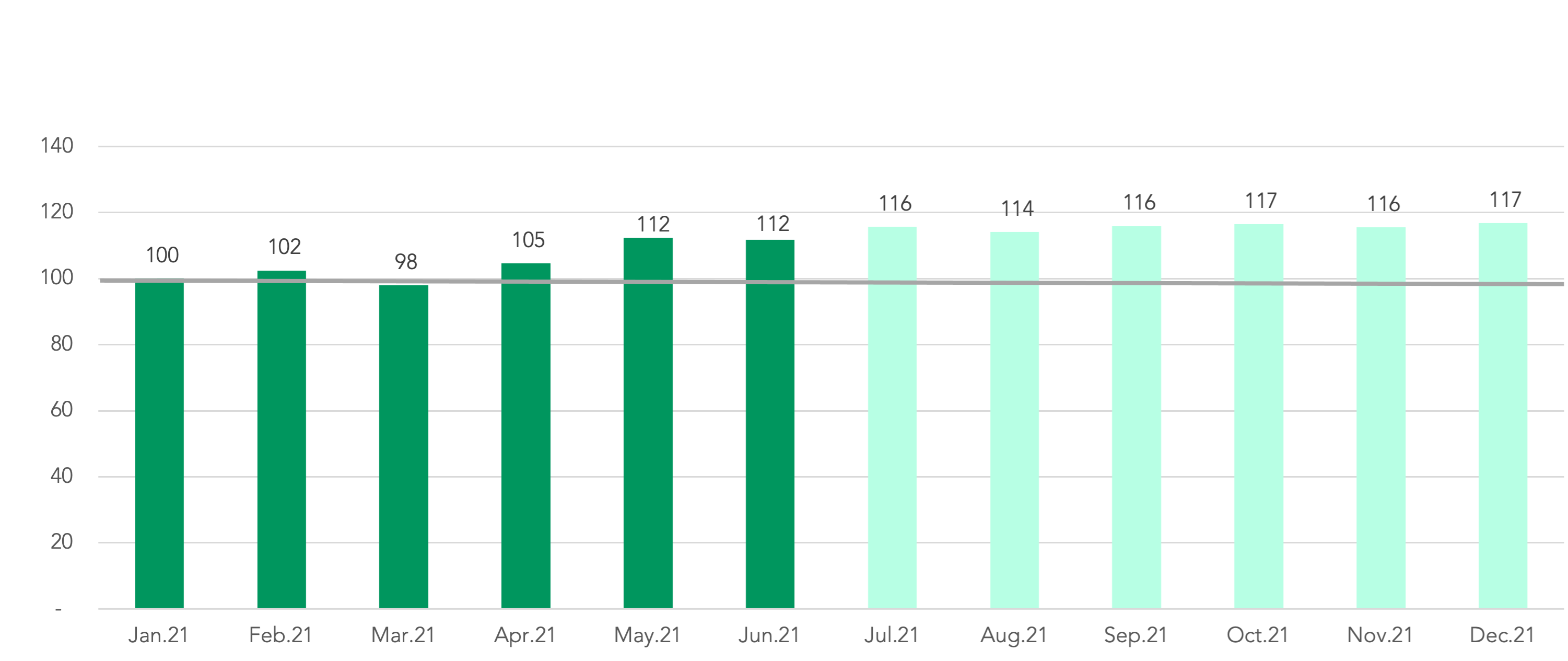

The answer lies at least partially in the excess liquidity in the deposit accounts of U.S. corporations. At the outset of the pandemic, when companies received an influx of low-cost PPP funds, much of that capital was parked in deposit accounts rather than utilized. Deposit balances continued to rise even as PPP loans were repaid, suggesting that many companies may be able to self-fund their expansion initiatives rather than going to the bank loan market. The rise in commercial deposit balances continued in 2021, as seen in Q2’s PrecisionLender data (Figure 2).

Figure 2: Could Excess Liquidity Hamper Borrowings?

Commercial Deposit Balances, by Month

Source: Q2|Precisionlender. Analysis reflects the aggregate commercial deposit balances for a cohort group of PrecisionLender clients, indexed to 100 for January 2021.

Signs of a Shift?

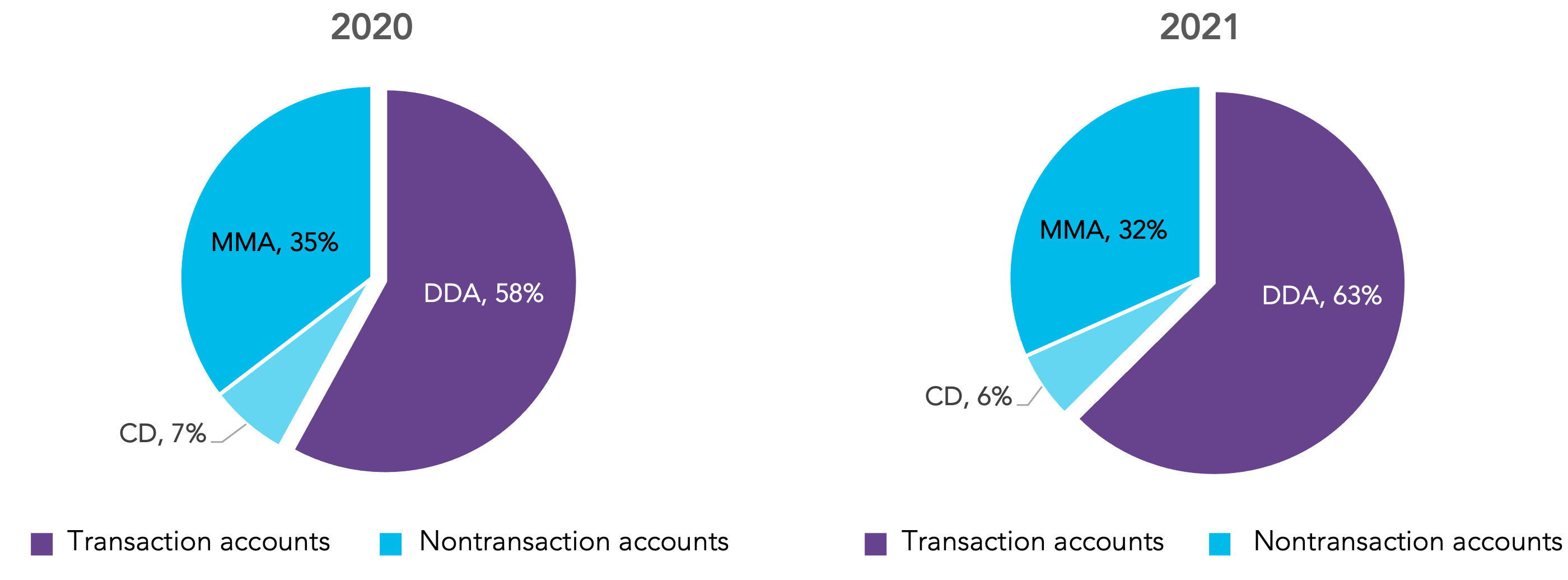

But conditions may be shifting for the better for commercial lenders. One signal that companies may be ready to tap into their deposit accounts and invest is the recent shift from money market accounts, CDs, and other non-transaction accounts into transaction accounts. While it is not uncommon for such shifts to parallel a decline in interest rates, which render non-transaction accounts less appealing, there has been a measurable influx into transaction accounts even since year-end 2020, long after rates were slashed (Figure 3). The relative rise in DDA balances suggests that companies may be preparing to utilize their funds. As those balances are used, increased reliance on bank funding should follow.

Figure 3: Deposits Shift to Transaction Accounts

Source: Q2|Precisionlender. Data was gleaned from PrecisionLender client data and reflects the percentage of commercial deposit balances held in the respective accounts as of year-end in the indicated year.

A Brighter Outlook for 2022

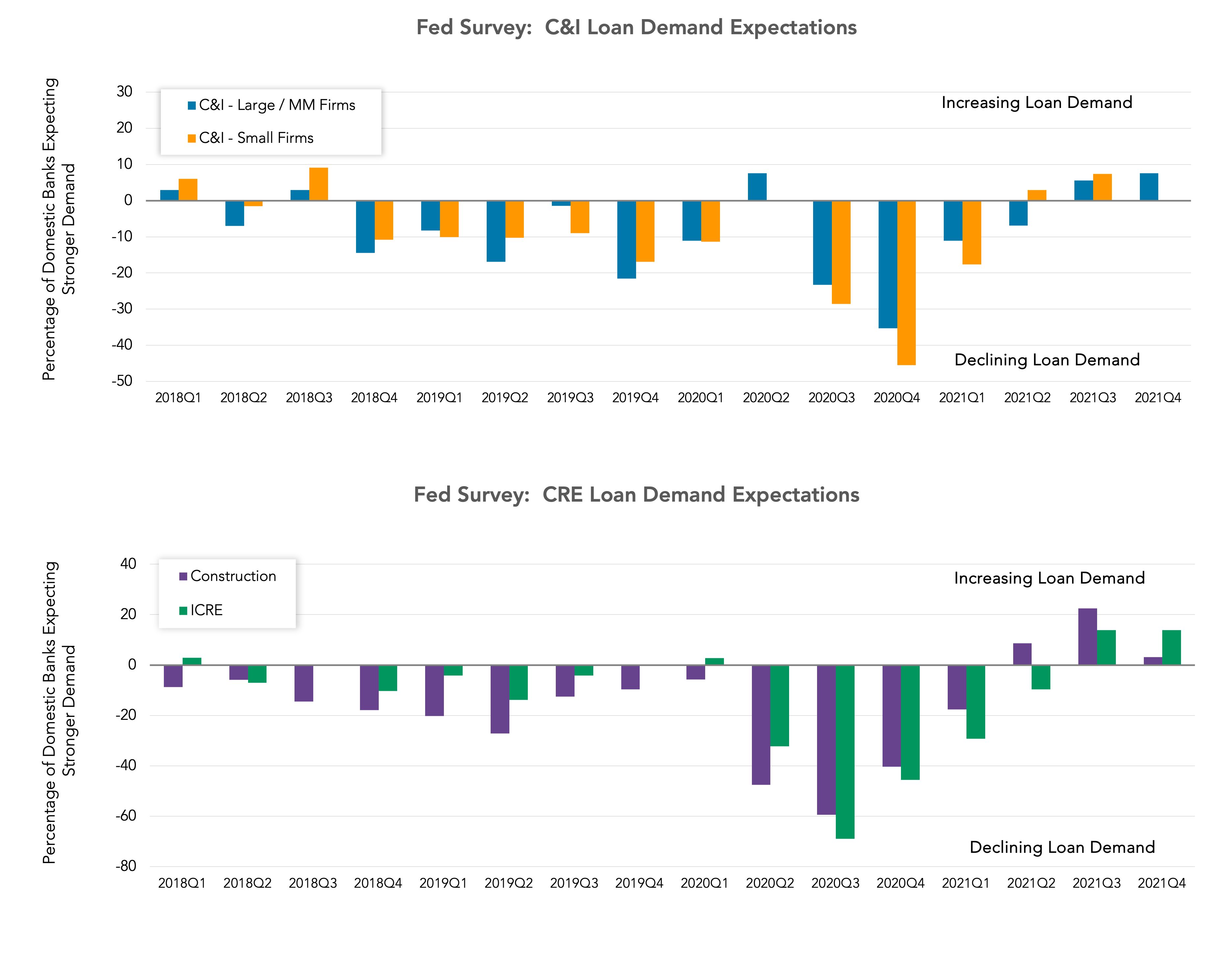

Bankers appear to agree that better times are ahead for booking commercial loans. In the latest Fed survey (Figure 4) bankers projected that demand for both C&I and CRE loans should rise modestly in the months ahead. They expect that loan demand will rise more for large and middle market firms than for smaller borrowers and will be comparatively higher on investor developer CRE than on construction deals.

Figure 4: Senior Bankers Project a Modest Recovery in Both C&I and CRE Loan Demand

Source: Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices

Source: Federal Reserve Senior Loan Officer Opinion Survey on Bank Lending Practices

Learn More

The shifting narrative on commercial loan demand was just one of the interesting findings that surfaced during our dive into 2021 commercial banking data. To learn more, make sure to register for our upcoming webinar, the State of Commercial Banking: Jan. 2022 Market Analysis.