Here are ways to lessen this threat

By John Merrill, Q2 Director of Product Management, Lending

Fraud rates remain “concerningly high,” according to Aite-Novarica Group’s 2021 Fraud in Small-Business Lending Impact Report*. Of the lending institutions examined, 18% stated that fraud was connected to more than 1% of their small-business loan portfolios – a significant worry. Probably more worrying, among the examined institutions, only 31% had fraud incidence rates that were negligible, which Aite-Novarica Group describes as “unsettling.”

This is a fitting description, given that fraud losses are usually always equal to at least 100% of the value of the credit commitment and right now, spreads (i.e., “the profits by which fraud losses are cushioned”) in the small and medium-sized (SMB) credit market are thin.

Among other Aite-Novarica Group findings:

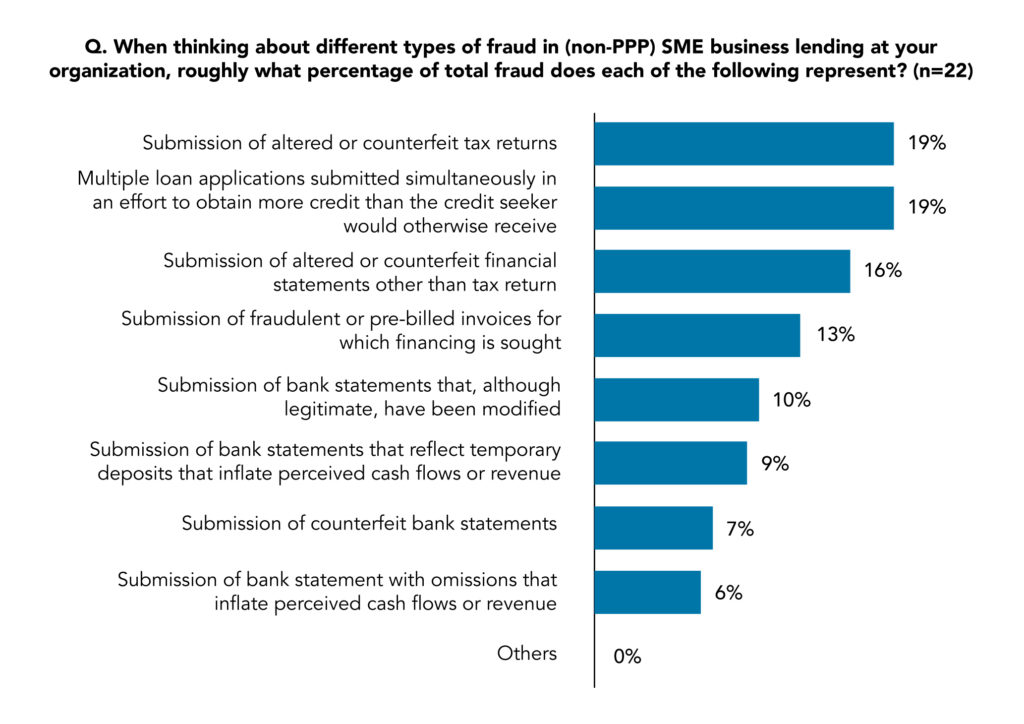

- The most “virulent fraud vectors” encountered by SMB lenders are loan stacking and document fraud involving tax returns, invoices, financial statements, and bank statements.

- Those most likely to be identified as the perpetrators of credit abuse or fraud in SMB lending are criminals using breached credentials and those committing fraud as a criminal enterprise and masquerading as a legitimate credit-seeking business.

- Among the fraudsters are legitimate businesses committing deception in pursuit of credit from an institution that would not otherwise extend it.

Loan stacking particularly stands out as trouble

Close to 20% of lenders surveyed cited loan stacking as a major concern. While the impact report found the ecosystem for SMB lending is becoming robust, built for scale, and has an easy borrower experience, reporting among agencies lacks standardization and is “dogged by latency.” As a result, a criminal enterprise masquerading as a legitimate business, or a legitimate business in need of funds and willing to commit credit abuse, can easily go undetected if it submits multiple credit applications during a brief time.

Lenders are fighting back against fraud, though. Digital helps.

Today, fighting lending fraud manually is ineffective – you need to apply better digital technology, data, and other information. Aite-Novarica Group points out that lenders have begun successfully summoning the technologies and best practices required to detect and deter credit fraud.

The research and advisory firm also stresses that fraudulent activity in SMB lending can be detected and deterred through:

- Access to fraud-specific analytics and talent.

- Collaboration across financial crime-deterring disciplines within an enterprise.

- Granular due diligence that targets fraud vectors known to be used by criminals.

- Better collaboration and resource sharing among lending institutions’ various departments focused on financial crimes -- fraud, money laundering, and cyberattacks.

Read more about Aite-Novarica Group’s impact report.

The importance of integration as a fraud preventer

At Q2, we agree with the report’s recommendation that more extensive use of readily available technologies, including APIs for accessing unalterable credit-seeker financial data and greater use of analytics, will better vet entities seeking credit as SMBs.

We also believe that lending institutions “integrate” their online banking and lending systems to lessen fraud risk. A focus on lending to your known customers is a much safer approach. By doing this, a lender can offer loans to businesses that they know and are already “authenticated” in their system. This approach is a lot more effective than looking at applications coming through lender websites.

Q2 places an emphasis on security

If your institution has concerns about rising lending fraud, consider learning more about the security and compliance approach behind our lending and other commercial solutions. We also invite you to contact us with your questions or comments about this topic of concern for many banks, credit unions, and other lending groups.