19 Mar, 2024

Non-bank lenders historically have provided several advantages over banks for small and medium-sized business (SMB) borrowers. They typically can offer faster approval and funding, more flexible repayment options, and less paperwork. From a broader economic point of view, non-banks can also cater to niche markets and underserved segments, such as women-owned businesses, minority-owned businesses, and startups. As a result, non-bank lenders are important for the overall economic environment because they fill the gap left by traditional bank lenders and provide more choices and opportunities for entrepreneurs.

So, what’s happening as we move through 2024?

To answer this question, let’s first look at two of the most critical factors for SMB borrowers: the interest rates being offered on new credit facilities and the availability of credit to SMB borrowers from the traditional bank lending market.

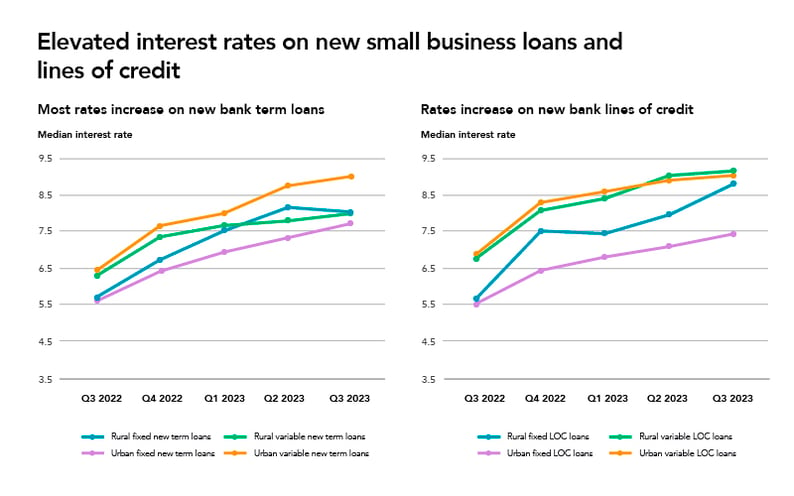

While many current headlines show that Fed policy has successfully slowed the rate of inflation, a report by the Kansas City Fed - published in late December 2023 shows that interests rates offered to small businesses on new term loans and new lines of credit continued to climb through Q3 of 2023.

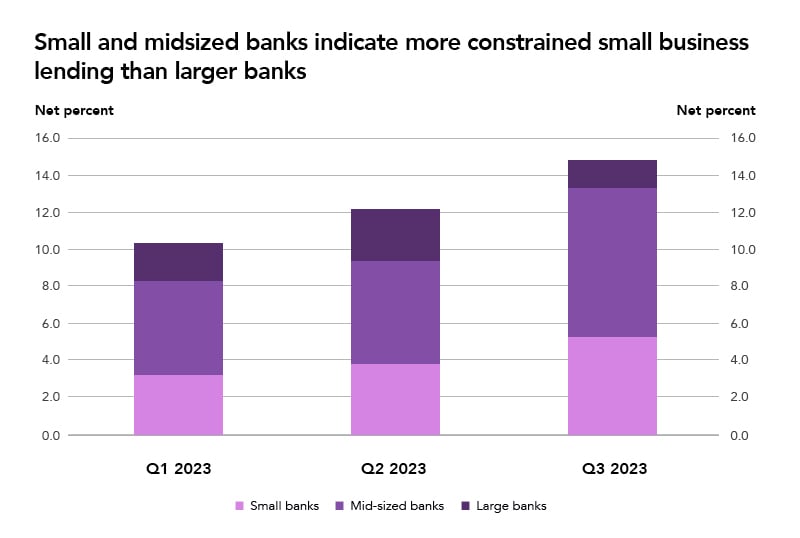

Perhaps more concerning for SMB owners seeking access to capital is the fact that more banks are feeling the pinch of a contraction in their liquidity and are responding with a more constrained lending posture toward the small business market.

The chart below from the Kansas City Fed shows not only a more constrained overall small business lending environment but also highlights the impact on SMBs—historically a mainstay for small business borrowers.

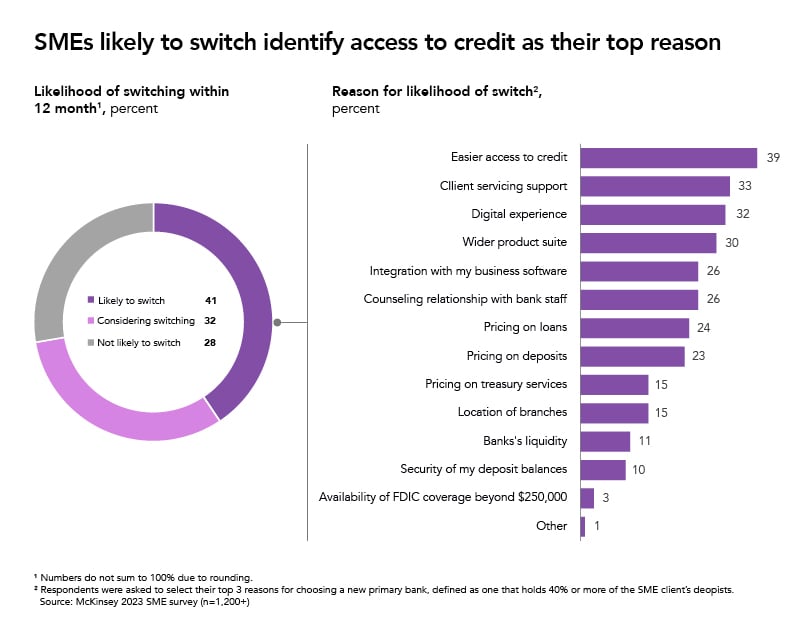

Are small businesses interested in switching from the banks they have been using?

This is the next factor for non-bank small lenders to consider. After all, borrowers must be interested in exploring additional relationships if they are going to capitalize on this opportunity created by banks’ interest rates and constrained lending posture.

According to a McKinsey & Co study from December 2023, an astonishing 73% of small businesses (referred to as “SMEs” in the study) are either “likely to switch” (41%) or “considering switching” (32%) over the next 12 months. Most important for non-bank lenders is that the No. 1 driver of switching is “easier access to credit”—as shown below.

How can non-bank lenders scale their operations (while maintaining margins!) to meet this market opportunity and fill the gap?

Fortunately, SMB lenders can be prepared to tackle this opportunity with a single solution: Q2 Digital Lending. Q2’s cloud-based platform streamlines the loan process for both the borrower and lender—resulting in a smoother, more satisfying origination and service experience for everyone.

Together, Q2 Origination and Q2 Loan Servicing:

- Simplify the application process, making application quick and easy for borrowers

- Deliver seamless CX improvement, providing loan decisions within minutes and reducing wait time for funding

- Reduce operational overhead and hands-on work by staff, allowing lenders to work within tight margins to cost-effectively scale their business

- Allow lenders to get their products—and product enhancements—to market faster

- Deliver easy configurability, creating loan processes that are flexible and scalable for lenders

From a borrower’s perspective, automated platforms cut down on the hassle of applying for a loan. They simply enter their data into an accessible, easy-to-use online application portal—no lengthy paper forms or in-office visits required.

Even better, automated approval decisions often arrive online in a matter of minutes, so borrowers know right away whether they’ve been approved for a loan and at what interest rate. Borrowers don’t have to wait days—or even weeks—for a loan approval.

Lenders, meanwhile, benefit from the platforms’ ability to cost-effectively automate and expedite loan processing operations. Q2 tools allow lenders to integrate precise, predetermined underwriting and approval parameters within their decision-making systems. As a result, the vast majority of loan decisions process automatically, without requiring staff review.

In this way, automation can help reduce the potential for human-driven data-processing errors and free staff to focus on the subset of specific, specialized loan applications that do require their hands-on attention.

A lifeline for small business lenders

Q2’s automated platform provides lenders with a practical way to not only bolster their underwriting but also fortify the overall health of their lending portfolios.

Using advanced credit scoring models and alternative data sources, such as bank account details and credit bureau information, Q2 Origination tools provide lenders with a comprehensive view of borrower creditworthiness.

Q2’s integrated, risk-based pricing strategies enable lenders to tailor interest rates and loan terms to the specific risk profile of each applicant, optimizing profitability while minimizing the potential for default.

Additionally, Q2 gives lenders access to built-in, third-party support tools that facilitate steps along the entire loan application and servicing process, including risk assessment, data accuracy verification, document signing, and loan collections, for example.

By building on the many added efficiencies these automation tools provide, lenders can scale their businesses and expand their lending portfolio—without the need to dramatically scale their staff size.

Even better: When lenders’ business growth or changing lending approach requires modifications to Q2’s automated platform, those can be made by any staff member. Unlike custom software modifications—which are expensive and may even require computer programming expertise—changes to Q2 platforms can be made more quickly and easily thanks to their low-code/no-code operational frameworks.

Do more for SMB customers and do more for your bank

By making the loan process easier, faster, and more efficient, lenders can bolster their efforts to capture profitability within challenging margins. Delivering better overall customer experience boosts opportunities for repeat customer business among the most sought-after, qualified borrowers.

Ready for a customizable, cloud-based solution that can help scale your SMB lending business efficiently and effectively? Elevate your lending operations with Q2’s best-in-class tools. Get started today.